In World Economy News 05/01/2016

Despite significant headwinds from moderating growth in China and expected US Fed rate hikes, economic expansion in the Asia-Pacific region will remain resilient in 2016, economist Rajiv Biswas tells DW.

DW: What is the overall outlook for the global economy and for Asian economies in 2016?

Rajiv Biswas: World economic growth is expected to show a modest improvement from 2.6 percent in 2015 to 2.9 percent in 2016, helped by gradual strengthening of growth in the advanced economies. However the global economy still faces considerable fragilities and challenges, with growth in many emerging markets having been hit by the slump in world commodity prices.

Emerging markets growth has slowed from 7.4 percent in 2010 to just 3.7 percent in 2015, with only 4.0 percent growth expected in 2016, as many commodity exporters face significant economic challenges from continued weak prices for key commodities, including oil and gas, coal and iron ore.

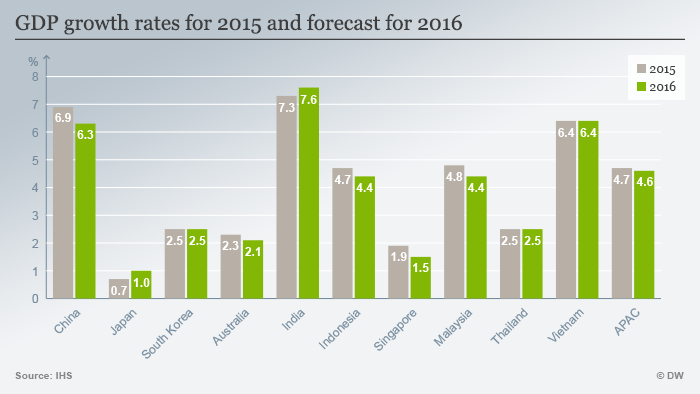

For the Asia-Pacific (APAC) region, despite significant headwinds from moderating growth in China and further US Fed rate hikes, the region’s economic growth is expected to remain resilient in 2016. Overall APAC’s GDP growth is forecast to be 4.6 percent in 2016, similar to the 4.7 percent rate estimated for 2015.

Which countries do you expect to be the big winners of 2016 and which do you think will continue to face difficulties?

Two of the APAC economies that are expected to perform strongly in 2016 are India and Vietnam. India has been a big winner from the collapse of world oil and gas prices, since India is heavily dependent on imported oil and gas. India’s current account deficit has narrowed significantly due to the lower cost of fuel imports, while Indian inflation has also slowed significantly, allowing the country’s central bank to cut interest rates.

In Southeast Asia, Vietnam has again emerged at the forefront of the fast-growing economies in the region, helped by rapidly growing exports of electronics and garments manufactures. Meanwhile, the two largest economies in APAC, China and Japan, continue to face significant economic challenges in 2016.

What will be the impact of further US Fed interest rate rises on Asia?

With further US Fed rate hikes expected in 2016, this will support the further appreciation of the US dollar (USD) against most emerging market currencies, including many Asian currencies.

Moderating Chinese growth and its transmission effects to the Asian supply chain may also trigger further capital outflows from emerging equity and bond markets. Asian corporate borrowers with large foreign currency debt, particularly in USD, could also face increasing stress if the USD rises further against their home currencies.

Chinese non-bank borrowers held an estimated $1.2 trillion of USD debt in mid-2015. The combination of moderating Chinese growth, excess capacity in key industries, rising USD yields and potential further USD appreciation against the Chinese yuan all create risks of further stress for some corporate borrowers, which could trigger an increasing number of corporate debt defaults in 2016.

Will China’s slowdown continue in 2016?

Chinese economic growth is forecast to moderate from 6.9 percent in 2015 to 6.3 percent in 2016. China is experiencing a period of significant adjustment and change as it makes the transition from a low-wage, export-driven economy to an upper middle income, consumer-driven economy.

This is causing painful and difficult changes in the manufacturing sector, as heavy industries such as steel and shipbuilding face major consolidation to reduce excess capacity. Meanwhile, consumer expenditure has become a more important growth engine, accounting for an estimated 54 percent of GDP growth in 2015.

Is there a risk of a China hard landing in 2016?

The Chinese economy still has many economic imbalances, including the slowdown in residential construction since 2013, excess capacity in some key industrial sectors, and the rapid rise of unregulated shadow banking loans between 2010 and 2014. Due to these accumulated imbalances, the risk of a hard landing in China over the next two or three years is estimated to have a probability of around 25 percent.

A key factor mitigating the risk of such as hard landing scenario is that the Chinese government has signaled that the medium term GDP growth target is around 6.5 percent. Consequently any further significant moderation in growth would be likely to trigger additional monetary and fiscal policy stimulus measures to maintain GDP growth momentum at around 6.5 percent.

With Japan recording another year of modest growth in 2015, can Abenomics succeed in lifting Japan’s economic growth rate?

Japanese economic growth is estimated to be 0.7 percent in 2015, rising to 1.0 percent in 2016. Despite the “three arrows” of Abenomics, Japan faces very significant economic headwinds, most notably from demographic ageing and high government debt level as a share of GDP.

With Japan’s population falling each year, the total size of the Japanese consumer market is shrinking, which is a major drag on Japan’s long-term potential growth rate. As I have discussed in my book “Asian Megatrends,” the falling population is also creating tremendous problems for Japanese society, with many Japanese municipalities facing economic and social decline due to their rapidly falling population.

With Prime Minister Narendra Modi having been in office for over 18 months now, how is the Indian economy expected to perform in 2016?

The outlook for India is positive, with economic recovery forecast to gradually strengthen from 7.3 percent GDP growth in fiscal 2015 to 7.6 percent in fiscal 2016.

With continued lower oil and gas prices in 2016, India is expected to continue to benefit from low fuel import costs and moderate inflation pressures. Meanwhile, the Modi government has been successful in ramping up foreign direct investment inflows as well as accelerating infrastructure investment. Manufacturing output growth has shown a gradual upturn during 2015, which is expected to continue in 2016.

How significant is the impact of the China slowdown on the Association of Southeast Asian Nations (ASEAN)?

While ASEAN exports have been impacted by the economic slowdown in China, ASEAN countries’ growth momentum is expected to be supported in 2016 by continued resilient domestic demand.

The frontier economies of Vietnam, Myanmar, Cambodia and Laos are still expected to be among the fastest-growing developing countries in 2016. Economic growth in the Philippines is also expected to remain strong, boosted by the fast-growing IT-BPO industry and strong worker remittances from abroad.

Indonesia and Malaysia have been hit by lower commodity export prices, but overall economic growth is expected to remain resilient due to firm expansion in private consumption and investment. Over the medium term, China’s “One Belt, One Road” Initiative as well as the creation of the Asian Infrastructure Investment Bank (AIIB) and Silk Road Fund will help to boost ASEAN economic growth, particularly through accelerated infrastructure development.